National Bank of Kazakhstan, regularly assures both Akorda and the citizens that de-dollarization of the economy and financial system is going well. Official statistics of the regulator on dynamics of tenge and other currency bank deposits seems to prove that. However, there is a big problem here that Daniyar Akishev and his subordinates try not to notice.

The issue is that dollarization, just as any macroeconomic problem, has two dimensions. The first has to do with what is going in people’s heads. The second deals with what they do and what comes out of it.

National bank’s surveys indicate a decrease in expectation of depreciation among the population. However, a decrease in expectation of devaluation and increase in the faith on tenge – are not one and the same. Thus there is an assumption that a decrease in the share of deposits of non-financial legal entities and physical entities in hard currency and an increase in share of deposits in national currency, is not as much a hope in tenge as a rational use of a possibility of making gains in financial market. As soon as there is a threat of currency devaluation, the pendulum will go back.

With this in mind, declaring that the problem of de-dollarization of Kazakh economy and financial system is being solved, is highly dangerous for the reputation of the National bank and its management. This is, especially considering that outside factors, such as hydrocarbon price hikes or US’s monetary policy under the new president can cause unexpected problems.

For example, what would happen to tenge-dollar exchange rate if the White House implements sanctions against Nazarbaev and his inner circle, and based on the verdict of American courts Kazakh equity of Kazakhstani officials and oligarchs will start being seized all around the world? Or how would tenge behave if Russia decides to weaken rubble against other currencies in order to solve a sudden issue?

The number of negative factors capable of undermining current stability of tenge against the dollar is pretty high, and a real stabilizing of the rate of the national Kazakh currency is possible only after a considerable decrease of the share of foreign trade in the GDP of a country. However, this can only be achieved through a dramatic rise of domestic production and lowering of imports. This seems impossible in the near future.

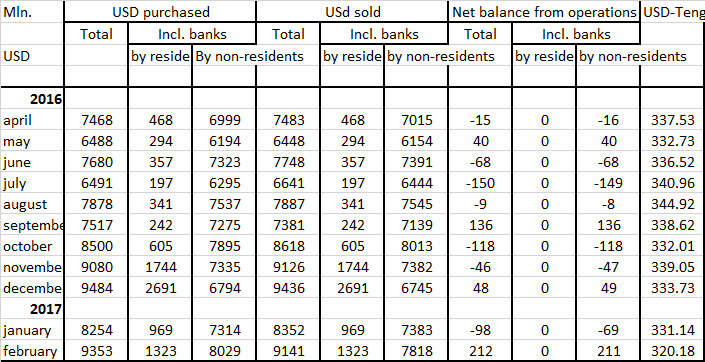

In conclusion, we want to note the situation at the off-exchange currency market, where at the end of last year and at the beginning of the current year there was a considerable rise in the amount of deals between resident banks. Considering there is no good explanation coming from the official Kazakh regulators, some fears arise.

Below, we offer you a table of the off-exchange cash flow of the American currency from Apr. 2016 to Feb. 2017. It is evident from the numbers that in Nov. and Dec. of last year the volume of buying and selling of US dollars was through the roof.

The situation has stabilized in Jan. of this year however, by Feb. of this year, this sector of the currency market, started experiencing some activity. Also, in Feb. of this year, for the first time in many months Kazakh resident banks, bought more dollars from non-resident banks, than the sold them – 211 mil. more. This is considering the fact that according to the National bank, the country is experiencing a surplus of both tenge and dollar liquidity; so it looks like the current de-dollarization of Kazakhstan is only until the first storm hits the currency market.