Almaty has hosted the XI annual conference of the Fitch Ratings agency on Kazakhstan, whose motto could be summarized as “today is a little better than 2014 and 2015”. This is probably why, on the eve of the conference the agency has confirmed country’s rating as the “BBB” with a stable forecast.

Three thematic roundtables were held as part of the conference: Forecast on the sovereign rating of Kazakhstan, Kazakhstan’s corporate sector and Kazakhstan’s banking sector.

Facilitator of the first expert discussion was Dmitriy Surkov – regional director on Russia and Black Sea region for Fitch Ratings. Before giving a word to main speakers, he spoke of being greeted on Kazakh land.

Turns out that in Almaty airport he was approached by a service dog, after which he was asked to show cash on hand. After stating that such dogs are usually trained to detect drugs, he was told: “this dog is trained to sniff out money!”. I smell of money! That is a good message – facilitator joked.

Does Kazakhstan smell of money? This is exactly what the experts were trying to find out during the first roundtable “Forecast on the sovereign rating of Kazakhstan”.

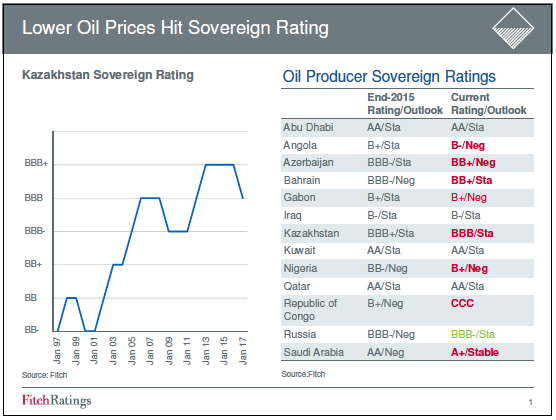

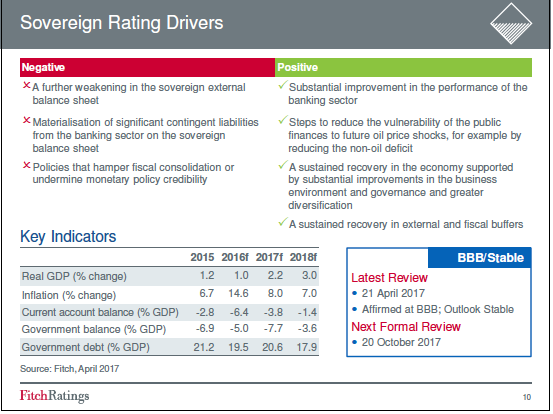

Discussion was opened by the director of analytical group on ratings of European countries with developed economies of the Fitch Ratings, Amelie Rou. She said that Fitch ratings has confirmed long-term issuer default rating of Kazakhstan in foreign and national currency at the BBB rating with a “stable” forecast. Ratings of priority debentures of the country in foreign currency are confirmed at the BBB level. Short-term issuer default in foreign and national currency is confirmed at the F2 rating. Rating of country’s ceiling is confirmed at the BBB+ level.

As follows from the report, prepared by analytical group under her guidance in advance of Almaty seminar, “Kazakhstan’s IDR, on one hand reflect a strong, state and foreign balance, which is bolstered by considerable government savings and net foreign asset of the government. On the other hand, they take into account a high dependency on energy-sector, weak banking sector and indicators of quality of management, as well as volatile macroeconomic indicators in comparison with comparable issuers with a BBB rating.

Moreover, there is a “continuation of a gradual adaptation of the economy to a considerable shock about oil prices in recent years, which is facilitated by the flexibility of currency rate, reforms of monetary policy, restructuring of banking sector and fiscal stimuli”.

As for the forecasts, the “deficit of federal budget according to IMF will increase up to 7.7% of GDP in 2017, relative to assessment level of 5.0% in 2016, due to recapitalization (which, according to estimates will represent a one-time budget expenditure at the level of 4.2% from GDP) of country’s largest bank Kazkomercbank. Recapitalization is part of the process, as part of which Kazkomercbank will be acquired by second largest bank – People’s bank of Kazakhstan”.

Fitch also expects that “decrease of deficit will be facilitated by higher oil prices, and bases its opinion on the lack of additional expenditures of recapitalization after 2017”.

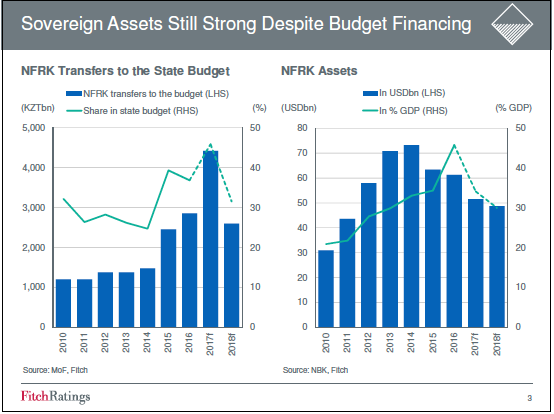

Balance of government budget, in Amelie Rou’s opinion, is very strong and “reflects asset of National fund of Kazakh republic at the level of 45,8% of Gdp by the end of 2016”.

Net government debt by the end of 2016 was minus 22.3% of GDP compared to median for comparable issuers at 33.1%. National fund of Kazakh republic will be used for partial financing of higher deficit in 2017, but Fitch expects that assets of the fud will stay on the level of above 30% from GDP throughout the forecasted period” – as follows from Fitch’s report.

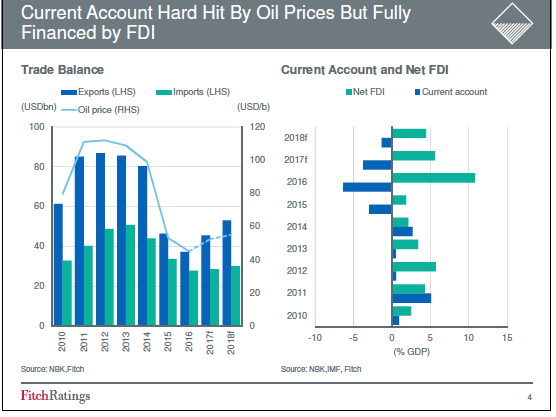

“Energy dependency is considerable, and lower oil prices led to a rise in deficit of current transactions up to 6.4% of GDP in 2016” – Amelie Rou’s report states. What follows from it is that oil export hasn’t experienced positive influences of decreased exchange rates due to economic hardships of major trade partners.

However, external prospects look good for 2017 and 2018, due to expected recovering of oil prices. Still, high imports related to direct foreign investments and outflow of income will ensure preservation of deficit of current transactions throughout the forecasted period. “Fitch expects that deficit will be fully financed through direct foreign investments that will remain significant, since the next year will see a expansion of oil extraction site Tengiz” – the report states.

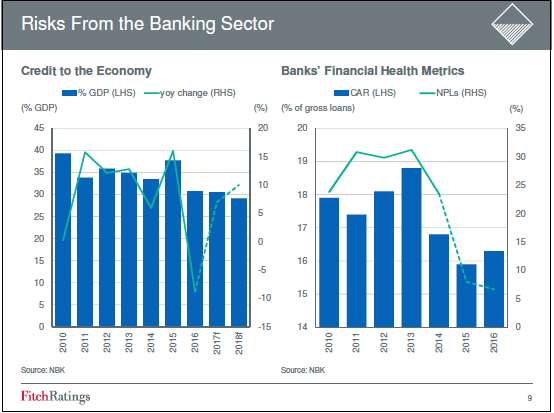

“Banking sector is very weak and has the indicator of banking system “b” based on Fitch’s methodology. The government as it looks, are aimed at restructuring of the finance sector, which is evidenced by Kazkomercbank’s support and intentions to conduct a quality assurence of assets in 2018. According to official data, problematic loans at the level of 6.7% from all loans, are considered moderate, but there is a chance of considerable undervaluation of restructured and distressed loans on balance of large banks that are partially backed by reserves. There might be a need for further recapitalization in the coming years, but Fitch expects that they can be managed relatives to the size of independent asset” – Fitch analysts say.

Overall, as follows from report, Kazakhstani economy in 2016 continued to adapt to devaluation of 2015 and lower oil incomes throughout last year.

“The rise in real GDP was 1.0% last year after a 1.2% rise in 2015, supported by the government program of anti-cycle stimulation. Fitch expect a rise in rate of growth of real GDP up to 2.2% in 2017 as the oil extraction increase (Kashagan oil extraction site has restarted its extraction works) preservation of high number of direct foreign investments and continuation of stimulus program. At the same time, even if the growing oil extraction and direct foreign investments, related to fuel-power sector presuppose more favorable mid-term economic prospects, preserving the dependency on energy sector means that macroeconomic volatility , likely will be higher then among comparable issuers in the rating category BBB, throughout the forecasted period” Amelie Rou’s reports states.

As for the management quality, we see its weaker indicators, based on World Bank’s methodology, on the matters of debt; moreover, revisions to constitution, passed this march, and aimed towards relegating parts of wide presidential powers to parliament and government, likely won’t lead to bettering of indicators, in short-term perspective, in agency’s opinion.

Among factors, that many negatively affect Kazakhstan’s ratings in the future, Amelie Rou sees a possible further weakening of foreign balance, materializing of considerable credit-related obligations, above those already stated, for the sovereign balance from banking sector, policy that may negatively affect budget consolidation or trust in monetary policy of the ruling powers.

Among positive changes in Kazakhstan’s rating are such factors as sustainable recovery of foreign and fiscal buffers, steps aimed toward lowering of susceptibility of government finances to drastic negative changes in oil prices in the future, for example, through decrease of deficit of non-oil budget, sustainable recovery of economy, facilitated by betterment of business environment and quality of management and higher diversification.

Sabit Hakimjanov, who had arrive at the conference with slightly late, started his report with the message that strong energy dependency of Kazakh economy, creates objective limitations within which we are forced to build our economic policy.

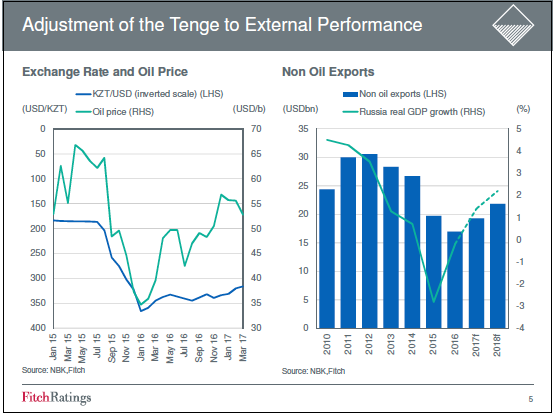

“The first factor that affects Kazakhstani economy is oil prices, second factor is the exchange rate of ruble. In the past 15 years, real exchange rate of ruble hadn’t deviated much from the real exchange rate of Russian currency” – said the director of department of financial stability and risks of National bank of KR, Sabit Hakimjanov.

However, as the representative of regulator noted, in the previous years there was a lag in change in the exchange rate of tenge after a change in rate of ruble. “These variations weren’t constant and they couldn’t be sustained for a long time” – this is how Hakimjanov explained the reason for devastating devaluation of national currency. “Now if you calculate the exchange rate based not on the price level, but on the salary level, you will see that Kazakhstan is at a historically most competitive level in relation to Russia. I.e. it’s at a level of 80%” – Sabit Hakimjanov assures.

He also expressed certainty that National bank will further stick to the policy of free-floating exchange rate of national currency. However, a flexible exchange rate cannot solve all economic problems. For their effective resolution, in Hakimjanov’s opinion, quality of institutes needs to be constantly improved.

By the way, those who were present in the audience had a lot of questions specifically for the representative of the regulator, however he unfortunately, wasn’t prepared to answer them.

After Hakijanov’s presentation, a discussion has started, during which, Surkov asked a question to the chairman of Citibank Kazakhstan Andrey Kurilin, who positioned himself in the beginning of the roundtable as not being a financial analyst.

Moderator asked him: Aside from the funds, that are already owed by the budget towards merging of two banks (KKB and Narodniy) do you assume that the government will face extra expenses for stabilizing of the banking system, in the coming years”?

To this question, Andrey Kurilin noted that this is a question is not for him – a market participant, but to those who run the country. In his words, situation, when banks might need help is possible, but its occurrence depends on many factors.

In other words, banker didn’t take on the responsibility to make forecasts, regarding what awaits Kazakh banking system in the future, and Dmitry Surkov had nothing left but to admit that he misses the target today, when asking questions to participants of discussion.

In the end, the impression was that all speakers are trying to politely avoid sharp angles, thus they didn’t dive too deep into problems, existing in Kazakhstani economy today.

All graphs and diagrams from speakers’ reports were built around comparison with indicators from 2014-2015, when economic situation was worse, in their opinion, than at the present moment. However, those present in the audience wanted more concrete information about what is happening in Kazakhstan’s economy today.

This was especially clearly voiced in the statement from the audience that disturbed peaceful flow of diplomatic discussion of problems in financial and economic spheres of Kazakhstan: “You all have described problems that exist on the financial market. But, when will the situation change? When will national bank take on a more flexible policy?” There was a silence in the audience, all of the eyes were aimed at Sabit Hakimjanov.

Representative of the National bank didn’t have an answer, however.