The hopes of reviving financial sector in Kazakhstan are put primarily on the government. Such conclusions could be drawn as a result of discussion of problems and prospects of the banking sector within the XI annual Fitch rating agency conference held in Almaty.

We talked about the country’s rating, forecast on the exchange rate of tenge and situation in large companies of oil and power industries in Fitch: a little better than yesterday and What is Kazakhstan’s corporate sector’s lifeblood. In this article, however we will talk of the prospects of Kazakh banking.

The session was opened by moderator James Watson, managing director of the analytical group Fitch Ratings on financial organizations.

Having noted that the sector is going through some rough times recently, he gave word to Roman Kornev, director of the analytical group Fitch Ratings on financial organizations.

The pitfalls of the banking sector

The speakers stressed the fact that Kazakhstani is starting a period of massive transformation, a result if which will be enlarging of financial institutes and their revival.

“We assume that risks for creditors in the present moment remain considerable, this has to do with high possibility of losses due to canceling of debt liabilities as a result of reorganization and in some cases liquidation of banks. A massive work on reinforcing of the surveillance functions of the National bank and bettering the standards for giving out loans by sberbank is expected.

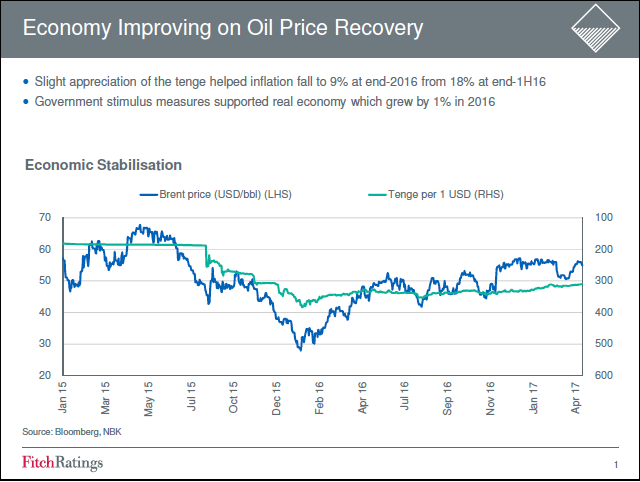

At the same time, in Kornev’s opinion, the outwards view of the banking sector is moderately-positive, which is due to relative revival of the oil prices and forecasts of their further strengthening.

Based on speaker’s data, Kazakhstan was able to avoid recession in 2016, there was a growth of economy, even though quite modest – 1%. In 2017 the growth will continue and will possibly be 2% which has to do with projects in the oil industry.

“Moreover, extensive stimulating efforts from the government, were a big support of the economy and a positive factor for the banking sector. In our opinion, these efforts will remain considerable in 2017” – forecasts Kornev.

Speaking of sectors problems, he named a considerable drop in real income of the population as a big problem.

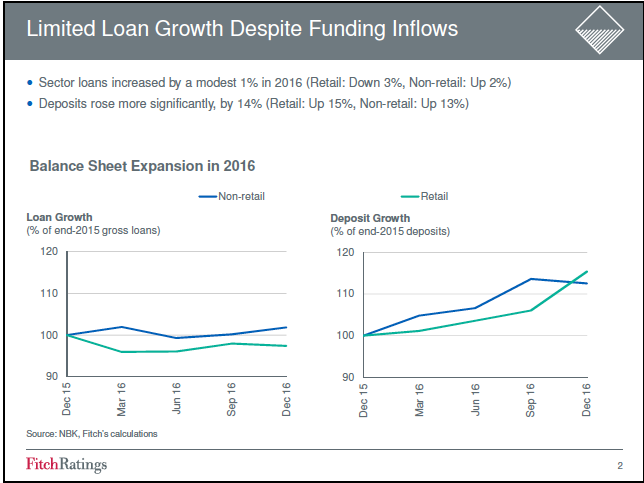

Stimulating efforts from government, have led to an increase in volume of money in the economy. For this reason, growth of deposits was 14% in 2016 and we expect that this growth will continue at a high rate in 2017. In the last year, this growth happened in the backdrop of modest growth of lending, total loan portfolip of Kazakhstani banks has grown only by 1%. At the same time, retail lending showed a decrease of 3%, which was related to writing off in large specialized banks. It was due to risks, that banks weren’t ready to take on, as well as high rates on funding of tenge” – Kornev described the situation.

“We expect a partial recovery of the growth of lending in 2017, – he further noted with a cautious optimism, – it will remain moderate and may reach 5% mark.” He explained that modest rate of lending in the past three years lead to accumulating of quite big volume liquidity among banks in 2016. “Banks mostly placed short term notes of the National bank of Kazakhstan, volume of notes today exceeds 3 tril. tenge, and this volume will continue increasing as a result of stimulating efforts from the government. At the same time, profitability from notes of National bank gradually decreased in 2016, and further decrease is expected.

Low quality of assets, remains another problem of banks.

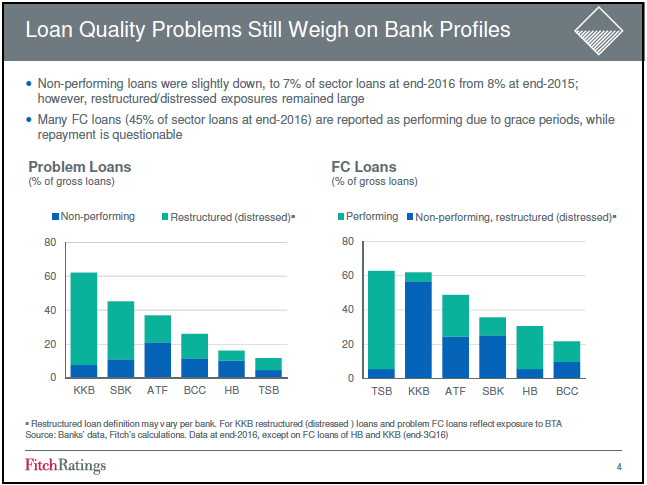

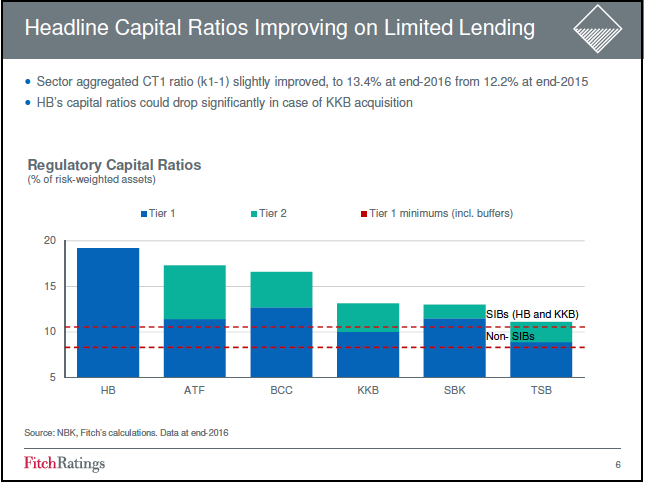

“Non-earning loans in the sector have somewhat went down to 7% mark by the end of 2016, and the share of non-earning loans comprised around 10%. At the same time problems of the banking sector are not limited to volume of non0earning loans – Kornev said. Aside from that, in the majority of banks, restructure loans comprise over 10%. In separate banks, for example Kazkom stress loans represented by the debt of former BTA bank exceed 60%.

Potential problematic assets, in our opinion are currency loans, which by the end of 2016 comprised 45%. But many of them are classified as earning. This has to do with the fact that quality and servicing of such loans is supported through grace periods on repayment of core debt, and in a number of cases, currency loans are subsidized by the government in such industries as agriculture and construction, which means that a part is payed off by the government.

In speaker’s opinion this isn’t in a long-term perspective, and problems related to quality of assets of currency lending may actualize.

As for total volume of problematic loans in the banking sector, kornev estimates them based on banks, included in agency’s ratings.

“Share of non-earning loans has comprised around 600 bil. tenge, which is a pretty considerable sum. However, much more, around 3 tril. tenge is comprised of the share of restructured or other stress loans. Around 80% from this portfolio is attributed to Kazkom, which has to do with it having former BTA bank’s debt. It isn’t hard to notice that a considerable share of currency lending falls on one bank – Tsesnabank, which at present time is the third largest bank in the system. Considering recent acquiring of large share of BankCentrecredite as well as keeping in mind, potential possibility of a deeper integration between these two banks.

Dedollarization continues

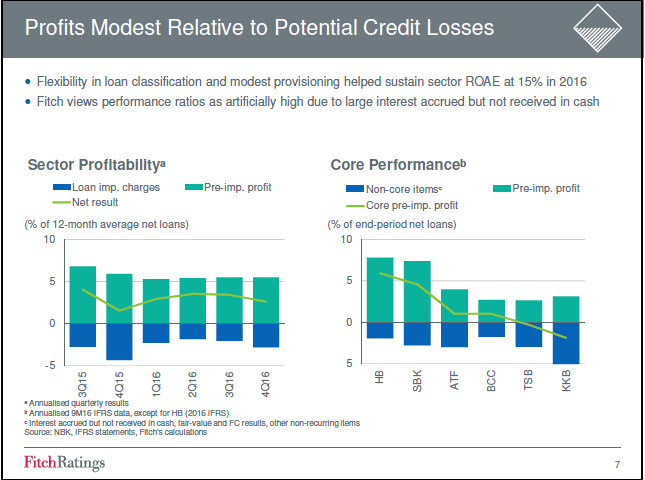

In speaker’s opinion, thesis on the overstated indices of the banking sector is related to indicators of profit.

Overall, aggregate indicator of profitability of the capital of banking sector for 2016 was 15% which is a high number. However, we think that this is largely explained by such factors as low volume of transfer s into reserves, low accumulation of problematic loans, presence in the structure of the banking profits that are accrued via accounting, but is not received in monetary funds. Such profits are considered low-quality and is part of secondary articles. Our analysis shows that with the noticeable exception of Narodny bank and Sberbank, four largest banks had the indicators of profitability corrected after deduction of non-essential items, it was close to zero or negative, – Kornev said.

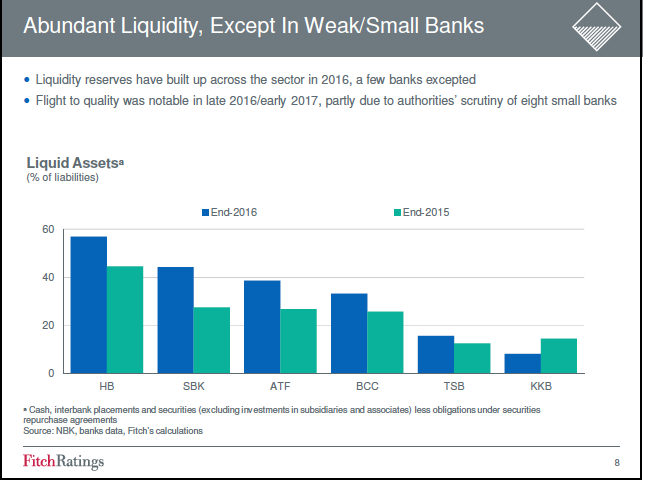

Speaker also noted that a strong suit of banks is still a high level of liquidity. “And such situation is seen not only in large banks, but also in small ones, there is a limited number of players in the sector that have low ratio of liquidit. And they will keep growing due to stimulus programs.”

However, in expert’s opinion, the transformative moment that started in Kazakhstani banking sector, will leave its mark.

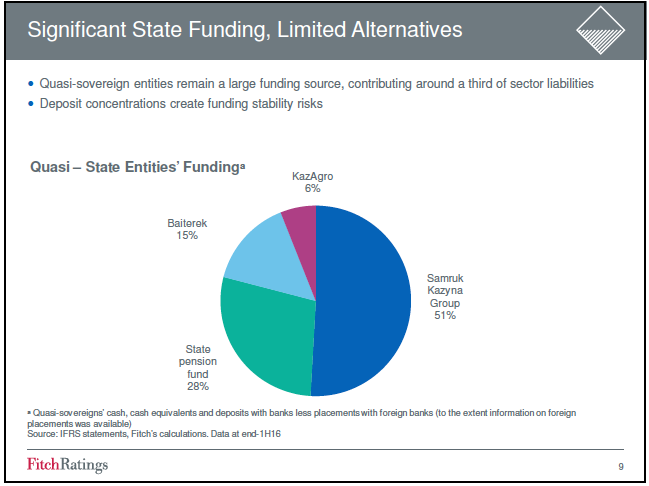

“In certain situations, especially in smaller banks it can lead to occurrence of stressful situations that we witnessed in the end of 2016 – beginning of 2017. When, based in our data, eight of the smaller banks had their inspections this caused negative reaction among lenders. As events of the beginning of the year showed, main factors, from the point of view of risk of banks’ liquidity are high concentration of funding and high dependency especially among smaller banks, from government funding. These are deposits and long-term loans provided by the group of companies Samruk-Kazina (51%), KazAgro (6%), Bayterek (15%) as well as bonds and deposits ENPF (28%). Based on our data, rate for government funding within obligations of banks is 30% and banks practically have no alternative besides lowering this funding ,” – Kornev emphasized.

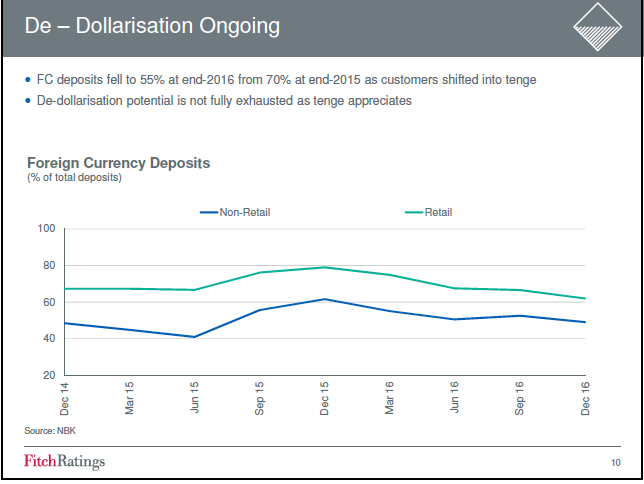

It was also voiced that dollarization within the sector continues. Currency deposits have shrunk down to 55% as of the end of 2016 from 70% (in 2015) and this tendency will remain.

Drawing concusions of his speech, Roman Kornev noted that at the present moment situation in many Kazakhstani banks remains difficult.

“Intentions to conduct positive changes have a moderately-positive impact for Kazakhstani banks. As we understand, the powers have drawn some sort of a plan on reviving of financial sector, but we weren’t able to see it yet. But based on a number of statements we can evaluate some of its outlines. First of all, it oversees strengthening of surveillance functions of the National bank.

As for financial component, as we understand, there is a plan to allocate funds fro the budget for cleaning of KKB’s balance within the framework of its acquiring by the Narodny bank, and this sum may be 3 tril.

As it looks, National bank positively views the process of banks bigger. But in our opinion, recovering of the sector is not only merging of banks, but some cleaning up of the balance and participation of stockholders in this process. Its not the first time that we meet at a conference and say that situation on the banking sector of Kazakhstan is dire. This is proved by the large volume of problematic loans, potentially problematic assets – currency loans, low capital buffers, weak opportunities for diversification of portfolio, which is related to concentrated economy; but one positive moment is a move to to recovery phase, even though banks’ ratings remain on the low level .These ratings reflect the fact that announced goals of revitalizing of the banking sector require effort.

Regulator shall help you

Deputy chairman of the National bank of KR, Oleg Smolyakov has focused in more detail on the plan of revitalizing of the financial sector.

“Last year was pretty significant from the point of view of changing of approaches, views of the National bank towards the problems of the banking sector. We came to an understanding that it would be a mistake to further postpone solving of the problems or to mask certain issues behind the financial reports. Thus the outlines problems are voiced and we are saying that the earning loans right now is over 7%, It is also obvious that around 15% of the loan portfolio is consisted of loans that are either non-competitive or bad. There are many such issues in the banking sphere that we determining during inspections.” – he said.

The next moment, in Smolyakov’s words is criteria of interconnectedness within legislation.

“The issue of economic inter-dependency for many banks is one of the main risk factors. We also understand that restructuring is not an absolute evil, i.e. unstable loans are also part of the business practice of bank’s lending policy. We also understand that IFRS allows for a wide range of auditor opinions that we see within regular inspections. This is at least 2-3 times the difference right now. This is just shows how subjective such an approach can be how differing and arbitrary it can be in relation to the real state of assets.”

Another important moment, in his opinion is the issue of funding.

“Its concentration in certain institutes is more pertinent, in others less so. And I agree that this issue cannot be solved quickly, thus the solution of this issue must be the increase of capital. By and large, all issues that were voiced, such the level of subsidizing of loans, economic inter-dependency, necessity of provision – all these issues demand a rise in capitalization of the banking system” – Smolyakov thinks.

In deputy chairman of the National bank’s opinion, we shouldn’t forget the fact that in the next 4-5 years there will opening of the borders within WTO and EAEU.

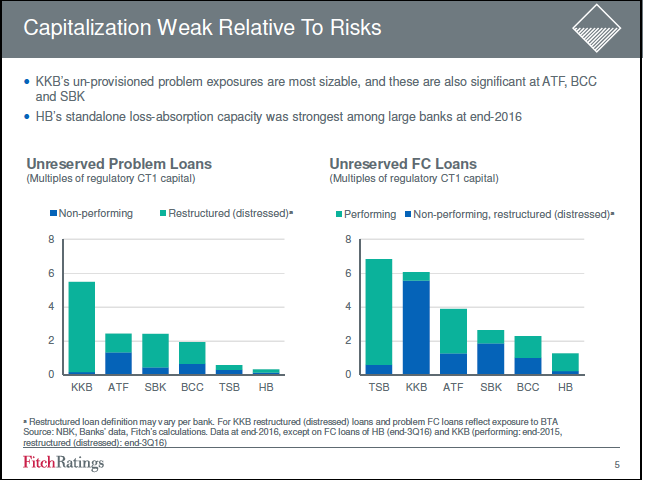

“There will be expanding of the issues of participation of institutes without commercial presence at the territory of countries. What needs to be done? Like we said capitalization needs to be increased. Right now, statutory capital ratio of first level, on average is about 14% within the system. But like I already mentioned, there are also over 7% of unearning loans over the 90 day mark; furthermore around 15-20% of restructured loans.

Sources of capital is one of the key issues. Here the basic principle of the National bank is that, it is impossible to support the bank without participation from stockholders – it would be profoundly wrong to use public funds without the desire and readiness of real possible stockholders.

Second source is increasing the profits. I wouldn’t view consolidation as purely physical process. Because within consolidation, not a single approval that National bank will put forward for merger, will not be based on some synergy taking place or expenses being cut; an increase in profitability is necessary, also through a decrease in expenses.

If needed, we are ready to implement a voluntary program for bank participation, i.e. if the stockholder presents the commitment for increasing of capitalisation of the bank, we are ready to present some temporary lending funds from our end” – speaker said of regulator’s plans.

Smolyakov later voiced the plans on revitalizing banks. “First principle is a regulatory tool, i.e. taking preventive actions before there will be an obvious deficit of capital. We think that the National bank has a way of evaluating ultimate economic beneficiaries. If the principle of economic inter-connectedness holds water, this will be grounds for National bank to take actions for reservation.

Second aspect is the regulatory provision; many of us lived in that environment, which carried distortions in accounting. We don’t want these distortions. This is why we are planning to introduce some adjustments to capital, to account for a gap between our understanding of stock depreciation and the volume of provision that we formed by the IFRS” he said.

But for this whole program to work, there needs to be a comprehensive plan of revitalizing of a bank, that is why we need to “essentially decrease problems on the active side of the balance, i.e. quality of loans and their inventory”.

In speaker’s words, all of the program participants will have to coordinate comprehensive revitalization plan with the National bank. “It will be long-term and will include a large number of actions. In case this plan will not be fulfilled during realization stage, National bank already has a warrant to use means of unlimited pressure, up to changing of managing team or demanding to do so from the bank” – deputy head of National bank warned.

In conclusion, he raised the subject of existing legislation for solving of assigned tasks on revitalizing of the sector.

“We see large number of gaps in the legislation. This is why this year we are ready to offer a new package of amendments in the legislation of the banking system. I want to emphasize that work in all directions and obviously solving of problems is impossible in one area. It is a process, when you implement a new approach, which can take not one month, but possibly years” – Oleg Smolyakov concluded.

Don’t expect too much

Deputy head of the board of the Narodny bank Murat Koshenov and chairman of the board of ATFBank Anthony Espina both took part in the discussion that unfolded after presentation of main speakers. First question from the facilitator was addressed to Mr. Espina and asked how a change in the landscape of the banking sector may reflect on a separate bank.

In his opinion mergers and enlargements carry both opportunities and risks. “I worked on Asian markets for many years: In Hong Kong, in China. Chinese say that the character of a risk consists of two parts. First is opportunities. Thus there is a risk for us, because two megabanks instead of four are created. At the same time we will have a number of additional opportunities: under consolidation, some clients will be able to receive loans which they hoped to receive from that bank, and will look for partners among other banks. Banks, in essence, will still be competing with us, and it is unlikely that much will change, whether there are 2 banks or 4”, – chairman of the board of ATFBank answered.

The next question, on the subject of credit recovery was asked by the facilitator to the representative of the Narodny bank; in Koshenov’s opinion the problem has two parts.

“First of all, borrowers must have an incentive to repay loans, i.e. act the right way and not look for technical and legal reasons and not go for a delay. The second aspect is that some lenders are unsecured, which is why banks often, even having won court cases cannot secure repayment of the loan. In that situation it is honest borrowers who forced to go through complicated procedures that suffer,” – he notes.

When the facilitator asked the question to all participants of the session about whether there are prospects for further lowering of the currency component of deposits a pause ensued, after which Murat Koshenov was forced to answer again.

“The dynamic in the past year in was positive in that regard. This has to do with the fact that there was a stabilization of the exchange rate. On the other hand a fairly large gap between deposit rates in tenge and dollars happened. It is worth noting that legal entities have reacted faster, and the share of deposits of representatives of small and mid-sized business in tenge has exceeded currency deposits. Physical entities, as a rule are more conservative and inert in their decision-making, though there was positive dynamic there too. But we shouldn’t expect strong dynamic this year. It depends on the rate of tenge which is affected by several factors, including outside ones: oil prices, as well as big influence of the exchange rate of ruble,” – he stated.

Then Mr. Espina got involved in the discussion again.

“In order to solve real problems in the banking sector, we have to evaluate macro-factors regarding assets, etc. It is worth noting that capital markets in Kazakhstan aren’t very developed. And if we, as a bank want to increase our capital we only have two sources: first is existing stockholders, and we have to have a developed base of both local investors and foreign ones as well as a stock exchange. It is one of the means of increasing the level of capitalization; we are talking about millions of dollars. I want to note that I am a banker by chance – my specialty is mergers and acquisitions, which is why these are my primary goals”.

Speaking on the subject of quality and quantitative growth of the loan portfolio of banks, participants of discussion concluded that a segment that grew last year by no more than 1% likely won’t result in much growth this year.

Let’s note that a lion’s share of questions was addressed to the representative of the regulator and had to deal with details and terms of realization of the program of revitalizing of financial sector.

Also they couldn’t pass the subject of the deal between Narodny bank and Kazkommercbank. “At some point published releases in which it was discussed that there will be a signing of memorandum between National bank, the government, Halyk bank, Kazkom and BTA; not much has changed since then, The bank is big enough and there needs to be big enough resources both from the bank itself as well as from the consultants. The inspection covers financial, legal and tax parts, and it is a pretty complex process. We expect the inspection to take about 2-3 months, and right now we are at the end of second month. Parallel to this there are talks on the aspects of the deal between various participants of the deal on its structure and rules; beyond that it is probably too early to say anything” – said Koshenov.

However, representative of the regulator decided to stand up for Kazkom. “I want to briefly add that just the fact that we are looking for a way out for Kazkom, and in our capacity as a central bank, provide it with necessary liquidity, is already a foundation to not look for possible negative scenarios. I want to also add that restructuring, including of the mandatory kind, not only of the external lenders but of the inner ones, isn’t the main one in the system” – he stated, answering the question of what will happen if in case

of a deal outside lenders will demand a prescheduled repayment of loans of Kazkom. Closing the session, facilitator tried to joke, by continuing the speech of the last speaker with the phrase “on this optimistic note, please let me finish our work”. There aren’t much reasons for optimism in the banking sector of Kazakhstan, from what it looks like, however.