Based on how quickly and orderly the Kazkommertsbank purchase by Halyk Bank is progressing, the deal is close to its completion which will, most likely, take place in the nearest time. As a result, a new super-bank will appear in the Kazakh financial sector, the bank that will own about two fifths of the assets, loan portfolio, and deposits of all the commercial banks in Kazakhstan.

At the first glance, this market monopolization seems random and unwanted, a result of the collision of different political and economic events, both external and internal, during the past decade.

Note that the problems in the Kazakh bank sector started in 2008 when the world economic crisis stroke and the outflow of capital from the emerging markets began. Then, there were Akorda’s political decisions on the devaluation of the national currency and on the nationalization of the two country’s systemic financial institutions, BTA Bank and Alliance Bank. The latter decision, as we see now, was incorrect on the system level, so the national economy suffered even bigger losses than they could have been, otherwise.

As a result of this collision of the political errors and the economic problems, out of the four systemic banks that, prior to 2008, had been fiercely competing with one another, only two have survived as of this moment – Halyk Bank and Kazkommertsbank. When the Kazkom purchase is completed, only one such financial institute will remain, the one belonging to Dinara and Timur Kulibayevs.

Note that, at that, the higher viability of Halyk Bank can be explained not only by a better management, a more cautious loan policy, a better marketing, higher rating, and the shareholders’ ability to increase the capital. There is also the fact that Halyk Bank has the best lobbying possibilities in the sector. We believe this is the reason Halyk Bank has always received a better support from the state, through the quasi-governmental agencies, in particular.

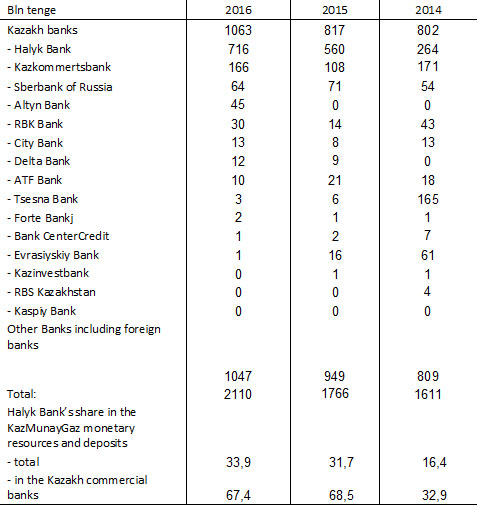

To support our thesis, we will cite a KazMunayGaz national company’s financial report. Below, you will find a table created based on the yearly group’s data on the checking account balances and deposits of the commercial banks.

The data clearly shows that Halyk Bank has the implicit advantage not only of the other Kazakh banks that have lower ratings but also of the foreign financial institutions whose ratings received from the international rating agencies are much higher.

As a result, for the past three years, the part of the KazMunayGaz group’s monetary resources on the Halyk Bank checking accounts and deposits have increased from 32.9% to 67.4% of the total volume of the monetary resources in the sector, therefore, superseding the bank’s share of the commercial banks’ assets, loan portfolio, and deposits by a large margin.

In total, the amount of the monetary resources that the KazMunayGaz national company and its affiliated structures kept in Halyk Bank as of the end of 2016 had grown from 264 bln tenge in 2014 to 716 bln tenge in 2016, in other words, by 2.7 times. At that, the total volume of the monetary resources on the commercial banks’ accounts, during this period, had grown from 1611 bln tenge to 2110 bln tenge, in other words, by 1.3 times.