According to multiple statements of the national bank of RK and explanations of its administration, including D. Akishev, abnormal activities of the regulator in the case relating to excess tenge mass, is caused exclusively by good intentions – such as lowering the rate of inflation and de-dollarization.

However, concrete results of the activity of the main bank of the country, makes one think that informally another goal is pursued – saving of the domestic banking system. To prove our version we prepared a brief analysis, based on the statistical data of regulator itself.

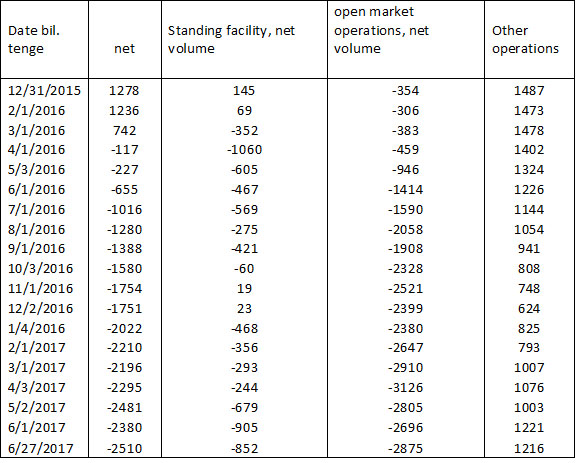

We offer your attention a table, prepared based on official data of the regulator, including the section “Open position on the operations of NBRK”. We made a selection based on the situation at the beginning of the month for the period from Dec. 31 of 2015 (earlier data is unavailable) until June 27 2017.

It follows from the statistic of the regulator that until the end of March of 2016, the debt of secondary banks to the National bank of RK exceeded the debt of the latter to them, and in April it reversed. And for 15 month already regulator is the net lender through standing facility and open market oprations.

At the same time it pays very high interest by global standards for the money lent money. We cite from the press release of the National bank of RK: “average-weighted profitability on the placed 7-day notes was 10.25%, on one month notes – 10.04%, on 3-months notes – 9.75% on 6 months notes – 9.68% and on 1-year notes – 9.45%” and “as a result of operations of the National bank in may 2017, average-weighed rate on 1-day REPO operations (indicator of TONIa1) set at the level of 10.07% (in April 2017 – 10.46%).

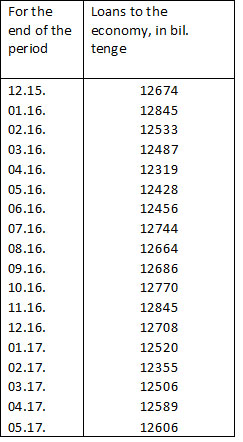

At the same time, lending of the economy by second-tier banks at the same period from Dec. 2015 until lat June, clearly stagnates, which evidenced by the data of National bank itself:

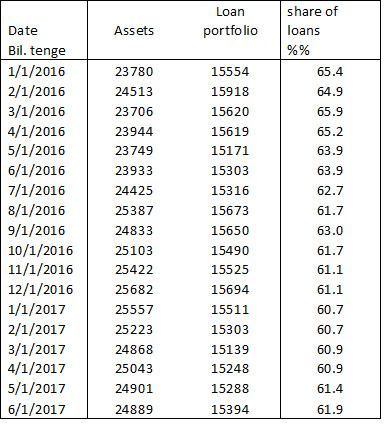

Below we offer another table in which there are statistic on all the loans of the second-tier banks, i.e. not only on the economy. Indicator includes (we cite): “Loans includes accounts in the category 1300 “Loans goven to other banks”, 1320 ‘Loans and financial leasing, provided to organizations, implementing separate types of bank operations”, 1400 “Demands for clients”, 1460 “Operations “reverse to REPO” with stocks”, without counting for corrections (accounts 1310,1311, 1324,1325, 143, 1431) discount and premium accounts (accounts 1312,1313,1330,1331,1432,1433,1434,1435) and accounts of provisions )accounts 1319,1329,1428,1463)”.

It clear from the table that the volume of assets of Kazakhstani second-tier banks, size of loanable package and the share of loans in the overall volume of assets in the last year has barely changed. And this is given the excessive tenge liquidity in the banking sector. The reason for why this happens lies on the surface: National bank of RK with its operations on tying up the tenge mass created a zone of heightened profitability, which given minimization of risks allows banks to make serious gains.

The question arises, why does the regulator do this? There is no economic sense in this tactic, since task of speeding up of economic growth of the national economy demands increasing its lending. However, National bank of RK understands or feels that the real economy isn’t ready for the growth of lending and in order to not allow spillover of funds into currency market and consumer spending, ties excess mass.

Also another explanation is possible. Current profitability of Kazakh second-tier banks without counting for operations with the regulator, is so low, and has so many problems, that National bank of RK gives them an opportunity to profit. But not for nothing, but in order to preserve, the appearance of prosperity, which doesn’t really exist. I.e. Akorda is saving not just Kazkom but entire banking system.