March 19, 2020, marked an unprecedented event that had never happened in Kazakhstan as far as we can remember — the National Bank of Kazakhstan and the Kazakhstan Stock Exchange (KASE) released a joint statement. So what’s at the back of it?

Here is this historic document (text in bold by kz.expert).

«Over the past day, the volatility on global financial markets increased significantly. The Brent oil price reached 25 dollars per barrel, decreasing by 14% over the day, and by more than 60% since the

beginning of the year. Global stock and currency markets continue falling. The Russian ruble weakened by 7,3% over the day, and by more than 30% since the beginning of the year.

Under these circumstances, in order to curb the destabilizing impact of external factors on the local currency market and for purposes of maintaining the financial stability of the Republic of Kazakhstan, the National Bank of the Republic of Kazakhstan together with Kazakhstan Stock Exchange JSC took a

decision to conduct trading in the currency pair tenge-dollar on March 19 and 20 in form of the Frankfurt auction.

The decision on conducting the trading in form of the Frankfurt auction will allow satisfying available client orders and preventing the situation on the currency market from destabilizing.

Updates on the further trading mode will be communicated via public statements».

The reason for this kind of unprecedented action on the part of the National Bank and the KASE undoubtedly lies in the critical state of affairs on the domestic currency market. By the looks of it, the number of the US dollar sellers has shrunk down to one (the National Bank of Kazakhstan) whereas the rest of the stock trading participants have turned into buyers.

Under these circumstances, the agency chaired by Yerbolat Dossayev has had three possibilities to choose from: a) to stop foreign currency trading until the world economic situation stabilizes; b) to preserve the market mechanism of the trading; c) to try and stabilize the exchange rate via massive sales.

As for the first scenario, the National Bank could not have carried it out. First of all due to the fact that it would have immediately started a panic on the domestic currency market and then the sales of the US currency at exchange offices would have stopped for a long time or were conducted at stratospheric prices while the citizens would have rushed to the banks to withdraw cash (tenge) or to convert the non-cash tenge into foreign currency.

Contrary to the Russian Central Bank, the National Bank of Kazakhstan could not have afforded to preserve the market mechanism of foreign currency trading either. Simply because, in this instance, it would have been doomed to sell, sell and sell.

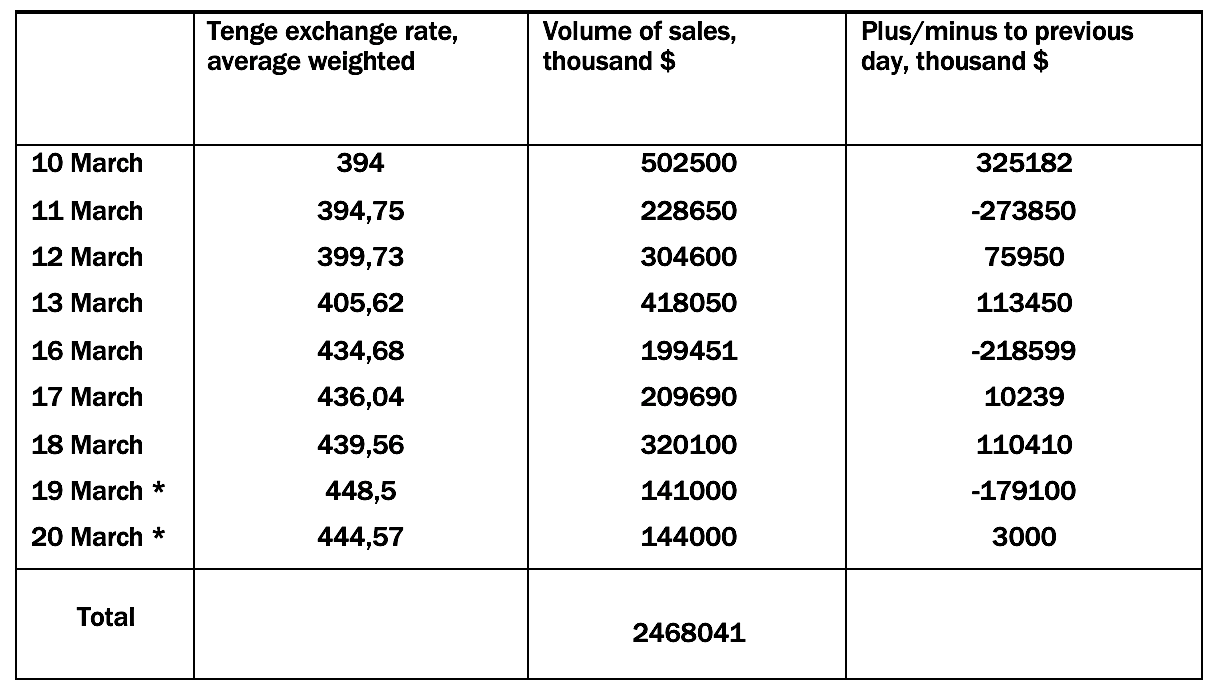

For this reason, the National Bank of Kazakhstan has chosen the third option (albeit not in its pure form but with the active use of the administrative recourse). To confirm our idea, let us cite the results of the KASE dollar tradings for the past two weeks (for the sake of convenience, we present them in the form of a table).

This table clearly shows that the total sum of the sales for the 9 trading days from March 10 to March 20 inclusively constituted almost US2.5 $ bln which, for the state, is quite a sensitive matter. However, the currency interventions would have been much greater had it not been for the employment of the Frankfurt auction by the Kazakhstan stock exchange on the order of the National Bank of Kazakhstan and for the hidden pressure exerted on the trading participants. And the fact that such pressure did take place is beyond doubt.

From the domestic policy standpoint, this means that, as the sole seller of the US currency, the National Bank of Kazakhstan is not so much selling it as it is distributing it among those striving to get the dollars. There is no doubt that this decision is a temporal and tactical one. By the looks of it, Dossayev’s agency is hoping that, in time, the craze (if not panic) on the domestic market will pass and then they will be able to make a further, more serious decision.

So far, we do not have an answer as to what this decision will be. Although it is obvious that the National Bank’s attempt to keep the dollar exchange rate at the 400 tenge mark has failed. Nonetheless, per fas et nefas, the state has managed to stop the falling of the national currency and then stabilize it within the 440-450 tenge corridor.

We are not to try and predict what’s going to happen next. But the very fact that, during the long weekend that coincided with the beginning of the Nauryz celebration, the exchange offices were mostly buying instead of selling the currency, shows that the tension remains.