At the end of October, Kazatomprom officially announced the start of the IPO proceedings at the London Stock Exchange. The Financial Times has recently informed the public that Kazakhstan’s national company intends to attract up to $600 mln and has already gained the support of the investors ready to purchase 15% of the shares.

The LSE trading session started on November 13 and will end on November 17. The investors will own 25% of the state company’s shares while 75% will remain in the hands of the current owner, National Welfare Fund Samruk-Kazyna. However, already at this point, we can state with certainty that Kazatomprom is now becoming a part of the international uranium complex and, from now on, the Kazakh uranium is to be kept in a secure place.

The Secrets of the Uranium Industry

If you want to know how the world’s uranium business and its biggest player Kazatomprom operate, you will find the answer in the publicly accessible investment Memorandum. This document of 800 pages is intended for the eyes of prospective investors and allows to understand the main features of Kazatomprom’s organization as well as its ties with the global market.

As we can see, Kazatomprom today is not just a company owned by the state. In the Memorandum, it is called “the national export and import operator in the field of the uranium, nuclear fuel, special equipment and technologies as well as the rare metals”.

The same document determines the company’s role as the representative of “Kazakhstan’s interests at the first stages of the nuclear fuel production cycle”.

The Controlling Minorities

The appearance of the new shareholders is going to bring serious changes to the company’s management system. First, they will have to adhere to certain rather strict procedures performed to avoid confrontations and may be even wars with displeased shareholders. And the recent development with the other Kazakh mining giant, Kazakhmys, when the quite an exemplary Kazakh corporation had suddenly become a pariah at the London stock market has demonstrated clearly that such a turn of events is possible.

One should be prepared for the fact that any internal conflict in the company may quickly transform into a public one (as dictated by the stock market rules). Information symmetry is the stock market’s sine qua non condition: all investors without exception must know about any existing problem.

The Memorandum states that the minority shareholders whose portfolio constitutes no less than 5% receive the special rights. For example, they have the opportunity to legally demand the compensation of the losses suffered as a result of the actions of Kazatomprom’s management. There is also the possibility to challenge in court all the major deals as well as the deals made with the interested parties.

Thus, some groups of the minority shareholders now have the possibility to control the making of all the strategic decisions and, in the case they are not pleased with them, to challenge them in court. In practice, it implies the unlimited possibilities to influence the making of these deals a priori and the necessity to include these shareholders in the perimeter of the operations.

In our opinion, this development is the key factor of the whole IPO deal. Strictly speaking, it means the Kazatomprom will become a part of the international uranium matrix – the system created in the recent years to replace the market.

Kazatomprom’s privatization has become the final step in the process of creating this matrix.

The Canadian Trail

We can understand how this matrix works by looking at the results of another IPO.

In July 2018, Yellow Cake plc held a public sale of the shares at the AIM market in London. ‘Yellow cake’ is how uranium oxide U3O8 used for the nuclear stations fuel production is called. Yellow Cake plc neither produces nor uses U3O8. This company has been founded for the sole purpose of buying the uranium from Kazatomprom and putting it in the storage warehouses.

In May 2018, before the Yellow Cake listing, a long-term agreement on these purchases was signed. But the purchases were made after the listing was completed and with the money received from the investors. The Kazatomprom Memorandum states that about 3100 tons of U3O8 (25.6% of the 2017 production) went to the Canadian storages. Then, there was another purchase so, as a result, the total sum of the 2018 deal constituted $180 mln.

According to the signed agreement, Yellow Cake has the right to buy U3O8 for $100 mln in the course of nine years. The purchasing price is defined as the market price, however, in 2018, it constituted $21.01 per one pound which is significantly lower than the spot market prices were at the moment of the operation’s completion. This fact had aroused some curiosity in the Kazakh media.

Amid all this, no one focused on the fact that it was Canada that became the end storage facility for a quarter of the Kazakh uranium yearly production volume. The storages belong to a plant located in Port Hope where they perform the uranium conversion. Once, this plant worked for the Manhattan project but, since 1988, it belongs to the Cameco corporation, the biggest publicly-traded uranium company and the second biggest company in terms of production size after… Kazatomprom.

Cameco, by the way, is one of the biggest players at Kazakhstan’s uranium field. Up until recently, the company owned the controlling stake (60%) in Inkay joint venture (40% of which belonged to Kazatomprom). After the lengthy negotiations, however, the shares had been reversed. In December 2017, they signed an agreement that sealed the company’s restructuring and now Kazatomprom owns 60% of it. On the other hand, the duration of the subsoil management contract has been extended to 2045. And now, as we can see, a quarter of the yearly production is accumulating in the company’s warehouses.

The Turbulent Market and Its Managers

So, without a doubt, Cameco acts as part of the big uranium market management scheme. And even though the times of cartels or syndicates have irrevocably passed (presently, only OPEC is operating according such a primitive model, however, the organization is forbidden to work in the biggest Western countries), to deny the existence of the directing force at the uranium market is pointless.

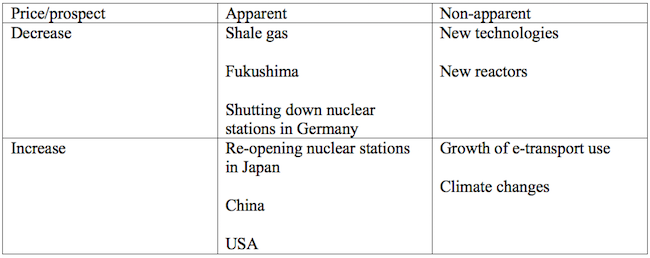

The uranium market is now operating in the state of turbulence and several factors influence its prospects simultaneously. All of them go for both the rise and the fall of the uranium prices. We will name only the most apparent ones (we will describe the interworking of the factors and the main players matrixes in a separate article – kz.expert).

The Matrix of the Uranium Market Factors

In these circumstances, it would be exceptionally careless to rely exclusively on the invisible market force, especially in such a special field. Therefore, it is reasonable to assume that it has its own “board of directors” searching for the legal instruments to influence the prices and finding them is the form of the purchasing companies such as Yellow Cake. Note that this is not the first publicly-traded corporation of this kind.

The first one was Uranium Participation Corporation (UPC), a Canadian publicly-traded company founded by billionaire Eric Sprott. In 2005, it too made an IPO at the stock-market. It was then when they established the rule – 85% of the sales proceeds was to be used for the purchasing of the uranium for the purpose of benefiting from the prices rise. Since then, the company has conducted 11 IPOs and received in total $765.2 mln from the investors. Such purchases look not so much like investments as attempts to balance out the market prices.

Note that UPC had made its mark in creating the Uranium One corporation but left the company when it was sold to Rosatom.

However, regardless of who is “pulling the strings” of setting the prices at the uranium market, the façade of this infrastructure looks impeccable. The purchasing companies, despite their satellite character, are listed at the stock-market and their boards of directors look quite respectable. They include the representatives of the business elite as well as the reputable insiders of the industry.

Now Kazakhstan too has found its place there.